It was in a discussion with Paul Druckman, CEO of the International Integrated Reporting Council (IIRC), last week that I experienced something of an epiphany. I now finally understood the IIRC’s 6 Capitals model and, as a result, realised I had probably written the first integrated report aligned with the capitals concept……..in 2006.

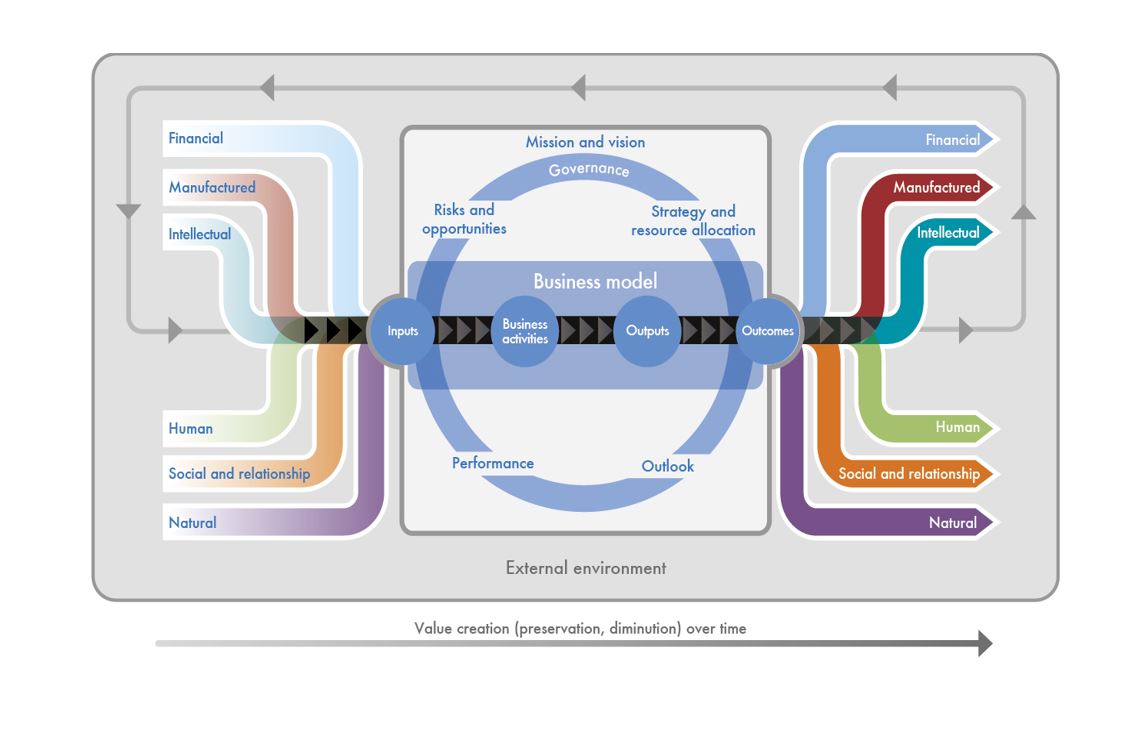

The 6 Capitals model is, in essence, an input/output model with an organisational black box at its core. That the black box has been illustrated to represent the value creating (or destroying) contribution of the business model is, to some extent, incidental. The basic premise is: resources in; add magic proprietary ingredients (choose a strategic or organisational management model); resources out, hopefully the outcomes being a higher combined (capitals) value than the capitals or resources that went in; and back round again for another cycle.

It is a very familiar concept. A similar model (not just in shape and structure) I have used extensively is the EFQM Excellence Model.

The EFQM Excellence Model emerged in the 1980s as part of a European response to the transformative growth of quality management (not to be confused with management of quality) in the US, as they learned from the traditions of Kaizen and the work of American management guru, W Deming, which had help fuel the post-war Japanese economic miracle. Fostered by governments and the European Commission, the European Foundation for Quality Management and its national satellites were originally a business led coalition but now extend well into the public and not-for-profit sectors. I think the EFQM still claims 30,000 organisational adherents which includes a number of the IR pilot companies.

When the European Commission issued its then seminal Green Paper in 2001 – Promoting a European Framework for Corporate Social Responsibility – I submitted a consultation response, on behalf of Lloyds TSB (where the EFQM approach was used extensively), suggesting the Commission shouldn’t seek to reinvent the wheel. The EFQM Excellence Model encompassed much of the growing scope of the CSR agenda – previously pigeon-holed, particularly in the UK, as corporate philanthropy and a bit of environmentalism – and could help embed in management orthodoxy. Sometimes, it seems that part of the agenda has barely moved on.

The response hit a nerve. I recall spending a day, by invitation, trailing from one Commission office to another meeting various officials including the then Commissioner for Industry’s chief of staff. It seemed the Commission were keen to see how CSR could reinvigorate their quality management policy! The least interested party was the EFQM itself; I think the then CEO thought CSR a distraction or, worse, a fad that threatened contamination of the hard won legitimacy of quality management.

But the EFQM did set up a working group, of which I was a member, to define the CSR application of the Model. I happen to think the resultant derivation of an EFQM CSR Framework had more to do with publication sales than progressing the generic model’s claims to be the answer to embedding CSR. The Framework is no longer promoted but subsequent changes saw ‘sustainability’ finally added to the governing fundamental concepts of Excellence.

However, at Lloyds TSB I adopted the self-assessment and continuous improvement change methodology which is at the heart of Excellence, creating an infrastructure which included a Board level steering group and a network of business champions embedded in line management and key functions.

Reporting is just one outcome of that process. In 2006, we issued multiple reports aimed at different audiences. There was a staff magazine pullout and 180,000 pamphlets in branches signposting our magazine-style 2005 Corporate Responsibility Review.

Lloyds TSB’s 2006 Corporate Responsibility Report was our ‘technical’ report for analysts and investors interested in the detail and data. It was explicitly structured on the EFQM Excellence Model.

Looking at it now, over 10 years on, I can see scope for huge improvement. And I don’t mean the design, inspired by a discussion with Mike Tyrell, now of SRI Connect but then a prominent sell-side responsible investment analyst. He convinced me that analysts didn’t want glossy reports but something stripped down that could be read in a taxi on the way over to the company meeting!

The real improvement would remove the CSR label, add statutory financials, and build a narrative storyline to more acutely link strategy, inputs, processes and outputs, illustrating with relevant data more effectively reflecting key performance and its impact on company value. In part, we could have monetised some of the non-financial performance impacts on business (financial) results. Otherwise, we might have used more material people, customer and society metrics. Above all, we could have better demonstrated how the processes transform resource inputs into output ‘capital’ growth. Then we would be moving towards what we now know as an integrated report.

Take, for example, people. As a resource (or as a subset, in IR parlance, of human capital) you would want to show why you employ the numbers you do, the complexion of skills and competences they bring and even their gender and ethnicity, especially where this is demonstrably material to your responsiveness to the customers and markets you serve.

HR and people processes – which should enhance skills and competences through learning and development – and the work culture and employment experience integral to employee engagement, will be reflected in labour productivity and organisational capacity for innovation. So the people results become better delivery and lower unit cost of products and services, higher customer perception and, ultimately, sales and profit. That last bit, the business results, should allow you to calculate a Return on Capital for your people processes.

Similarly, the combined contribution of people and other resources as factors of production, a mix determined by issues around access and availability and bounded by strategy and available budget, will define the effectiveness and efficiency of the production processes. That will show in production metrics like Six Sigma and Lean although the former often incorporates assessment of relative performance against customer expectations identified in ‘Voice of Customer’ analysis.

Improving or developing new processes, products and service, where designed to meet or even exceed customer expectations, will drive higher customer perception in metrics like Net Promoter Score (NPS). NPS and reputation with wider stakeholder groups, particularly those who influence customers, also incorporate the impact of externalities like the environment where they are not already a cost of production. The customer results should reflect customer satisfaction and loyalty in churn rates, and brand consideration and advocacy in market share. Ultimately, the business results are sales, net margins and earnings, the key ingredients for analysts’ evaluation of market value.

The logic flow of the EFQM Excellence Model helps make sense of the IIRC’s 6 Capitals model black box. It provides a platform for a narrative – and assigning relevant metrics – to articulate the contribution of strategy and processes to input transformation and the resultant outputs. The labelling of the models is different but the essence is broadly the same. That said, in the Excellence Model, business results (probably coterminous with IIRC’s financial capital) are the uber output.

The Excellence Model was a significant influence on the work of the European Commission-inspired Laboratory on Valuing Non-Financial Performance which I co-lead. The Lab’s VNFP model was the starting point of Project Delphi, in which I am currently engaged, which has gone on to develop a set of broad ESG factors and largely quantitative and material metrics, by industry, connected to a proprietary value driver model. The Delphi Framework and the EFQM Excellence Model share common ancestry. It should come as no surprise, therefore, that the Delphi Framework and the IIRC’s 6 Capitals model have significant synergies with the Delphi Framework delivering ‘Capitals’ relevant factors, metrics and the necessary supporting narrative.